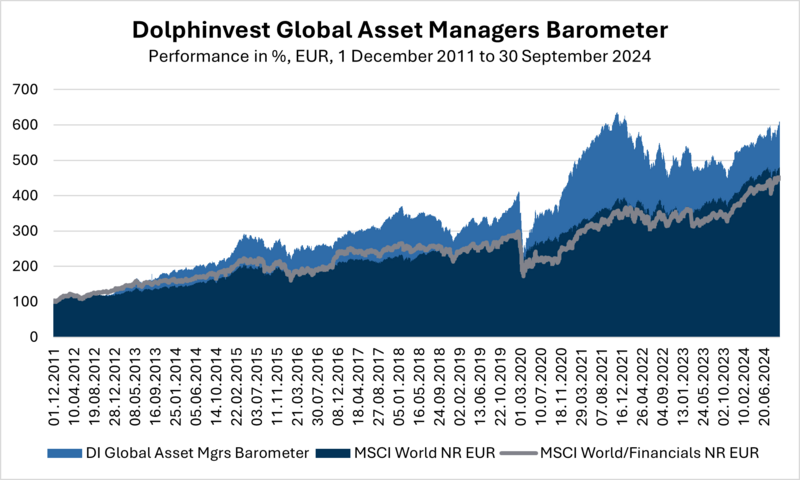

Dolphinvest Global Asset Managers Barometer

Asset management: A lot of catching up to do in the EU

The German government is planning to introduce a capital market-based old-age pension concept that seems almost revolutionary by local standards but can probably be better described as run-of-the-mill when compared internationally. Just like the Nahles pension plan previously proposed, the new ‘Altersvorsorgedepot’ is about motivating citizens to invest in capital markets – without a safety net or guarantees, but with the prospect of attractive returns. Citizens are supposed to be given an opportunity to top up their income from the state-run pension scheme by generating returns from capital investments.

The Nahles pension plan failed due to a lack of acceptance from employees and employers. The German government is now trying again and providing two incentives with its ‘Altersvorsorgedepot’: It is granting tax exemption on the investment income during the savings phase and is subsidising the saved amount by up to EUR 600 per year, which is several times greater than the basic allowance of EUR 175 for the Riester pension plan. This is not a trivial amount.

Meanwhile, the EU Commission is planning to turn the incomplete Capital Markets Union into a Savings and Investments Union. The initiative is commendable insofar as it sees private clients no longer just as taxpayers and consumers, but as investors who shall also participate in the economic future of the European Union.

By spreading the financing risks onto broad retail investor shoulders, the new Brussels-based initiative makes considerable progress towards achieving the goal of a capital markets union. Essentially, it is about breaking the outsized dependency on banks for corporate financing to better protect the real economy and governments from financial crises.

The US has certainly made more progress in this regard. There, the clocks don’t actually run faster – the US simply recognised 50 years ago that it was time to act. Companies in the US raise more capital in the markets than from banks (e.g. at a ratio of 75% to 25%, according to estimates of the Hertie School), while the reverse is the case in Europe (25% to 75%). The capital markets on both sides of the Atlantic are therefore worlds apart.

Size and growth

The capital markets of the US and the EU obviously differ in their size. Even though the EU outdoes the US by 30% in terms of population size, the US capital market is many times larger than its counterpart in the EU. The capital market size determines the size of the asset management industry, as this is the key service provider on the buy side of capital markets.

There are currently four publicly listed asset managers in the European Union whose initial public offerings took place at least five years ago, meaning they are established. With a market capitalisation of more than EUR 1 billion (based on Q2 2024 figures), they are also of considerable size. These asset managers are the two Italian companies Anima and Azimut, the French company Amundi, and DWS in Germany. In the US, the equivalent group of asset managers is comprised of 18 asset managers, including BlackRock, Blackstone, Invesco, Templeton, and Cohen & Steers.

Consequently, there are “only” about 4.5 times more asset managers in the US than in the EU that fall into this category of market participants, even though the US capital market is much larger. For example, the total capitalisation of all companies listed in the MSCI USA Index is seven times greater than that of the companies in the MSCI European Union Index. In other words, the average asset manager in the US manages more financial capital.

There are reasons for this. The EU still consists of 27 local capital markets and is therefore miles away from the efficiency advantages of a capital markets union. However, more than anything else, it is probably the much bigger tax incentives for non-state retirement planning in the US that have positively impacted the growth of the US capital and asset management markets in recent decades.

Contributions to a 401(k) pension plan are fully tax-deductible under US tax law and are considered special expenses – just like in Germany – thereby reducing one’s taxable income. In addition, taxpayers in the US benefit from a tax exemption for the portion of their wages that is paid into the 401(k) plan, currently up to a threshold of about USD 20,000 per year.

The first 401(k) plans came onto the US market in 1978. By contrast, the state-subsidised Riester pension plan in Germany has existed only since 2002; the Rürup pension plan since 2005; and the Nahles plan – along with its purely capital-backed pension plan without guarantees – only since 2018. Germany lags the US when it comes to developing a non-state pension system, both from a temporal perspective – namely by several decades – and in its implementation and acceptance. For example, the Nahles plan, which comes close to the concept of the 401(k) plan – is mostly rejected by employees and employers. By contrast, around 80% of US employees have access to a 401(k) plan, and almost 80% of these people make use of it.

Comparing profitability

In a five-year comparison from Q2 2019 to Q2 2024, the capital and asset management markets grew on both sides of the Atlantic but – hardly surprisingly – to varying degrees. In the second quarter of 2019, the four EU asset managers that were mentioned above generated total revenue of EUR 1, 517.8 million and income before taxes of EUR 628.2 million in total. In the second quarter of 2024, total revenue amounted to EUR 1,880.8 million, while income before taxes amounted to EUR 979.5 million.

In other words, the four EU asset managers increased their total revenue by 24% overall during this period, and income before taxes even increased by 56%. Amundi’s profitability – expressed as a ratio of income before taxes to total revenue – remained stable at 50%, while that of the other three asset managers improved.

The situation was different in the US, where total revenue of the 18 asset managers grew by 40% – much stronger than in the EU – while total income before taxes increased by only 29%, which was much less than in the EU.

The top five US asset managers with the largest share of total revenue offered an inconsistent picture: BlackRock’s market share remained stable; Franklin Resources gained slightly; while T. Rowe Price and Invesco lost market share. The largest gain, as expressed in percentage points, was achieved by Blackstone, followed by Ares Management and Hamilton Lane, all of which are providers of alternative investments.

While EU-domiciled asset management companies over the past five years clearly focused on boosting efficiency and profitability, their counterparts in the US concentrated on growth. The US asset management market distinguishes itself particularly through the development of new business areas in private markets, in which comparatively high revenue can be achieved from management fees.

Market capitalisation trend speaks volumes

Asset managers were also ahead when compared with other financial service providers in the US. In the 10-year period from 2014 to 2024, publicly listed asset managers in the US experienced the strongest growth in market capitalisation compared with banks, insurers and specialty finance providers.

However, this positive performance of the asset management industry in the US is solely attributable to the meteoric rise of alternative asset managers. While the total market capitalisation of US financial stocks increased by about 50% during the above-mentioned period, the market capitalisation of publicly listed alternatives providers rose by a good 350%. Listed traditional asset managers, on the other hand, brought up the rear in the universe of US financials, with a gain of 0 percent.

Despite the dire need for investment in Germany’s infrastructure, the ‘private capital markets’ theme does not appear in the details that have been made public so far regarding the new ‘Altersvorsorgedepot.’ And despite the negative experiences due to lacking or inadequate tax breaks and other financial incentives in the EU fund vehicles EuVECA and ELTIF, the EU Commission is making no recognisable effort to change anything in the deficient incentivisation structure. In Brussels, discussions are more focused on the question of whether a centralised regulator is better than 27 national ones, or the other way around, although Mario Draghi recently – and quite understandably – spoke out in favour of the centralised approach. That at least provides some hope.

Shareholdings and stakeholders

The US also differs from the EU in the shareholder structure of publicly listed asset managers. The biggest shareholders of the four EU asset managers are mostly banks and insurers as well as governmental and government-affiliated institutions.

This stands out most clearly in the case of DWS. Around 85% of the company is held by Deutsche Bank, Nippon Life and Norway’s sovereign wealth fund, with the lion’s share allotted to Deutsche Bank with around 79.5%.

A similar picture emerges with Amundi: A good 70% of its equities are held by 39 regional banks of Crédit Agricole (68.9%) as well as Amundi employees (1.4%).

Anima’s shareholders include the Italian government (12%) and Banco BPM (22.4%), while Azimut is partly owned by Norway’s sovereign wealth fund (1.7%) and the trust company Timone Fiduciaria (20.5%), which is 95% owned by another trust, Cofircont.

The shareholder structure of asset managers in the US is somewhat different. Here, it is primarily the funds and ETFs of Vanguard and BlackRock that have significant investments in asset managers. Often enough, these competitors are – unlike Vanguard and BlackRock – asset managers with an active investment approach.

Through its funds, Vanguard is the largest or second-largest shareholder in 12 of the 18 US asset managers that were analysed. The company’s largest shareholding is its 12.7% stake in Virtus Investment Partners (source: LSEG, as of 28 August 2024). BlackRock, with its fund investments, is the largest or second-largest shareholder in seven of the 18 asset managers. BlackRock’s biggest shareholding is its 14.1% stake in Artisan Partners (source: LSEG, as of 28 August 2024).

Together, Vanguard and BlackRock are the largest and second-largest shareholders, respectively, in five US asset managers, with combined shareholdings of between 15% (Hamilton Lane) and 26% (Virtus).

Demand for stewardship

It’s hard to believe that shareholdings of this kind can’t lead to any conflicts of interest. There is also the question of influence over competitors, and ultimately of a market structure with a monopolistic tendency.

The public demand for ‘stewardship’ would be such an example of influence: For example, proponents of this demand argue that fund managers should actively engage with target companies to achieve a sustainable benefit for the economy, environment and society at large.

Finally, the question also arises about risks to the industry. What are the implications for the equity prices of publicly listed asset managers if there are massive outflows from Vanguard’s and BlackRock’s large funds and ETFs? Ultimately, it is then a question of systemic relevance: Whether, and to what extent, risks to the entire financial sector – and therefore indirectly to other parts of the economy – emanate from an equity price slump in the asset management industry?

The Norwegian sovereign wealth fund, considered the largest in the world, held stakes in 18 of the 22 US and EU asset managers cited above, with around USD 3.5 trillion invested in total, at the end of the second quarter of 2024. The allocation has a strong US bias, and its largest EU positions are Azimut and Amundi.

Silver lining?

The short-term performance of the current year confirms the edge that the US asset management industry has over its peers in Europe. However, a look back over a longer period shows that European asset managers outperformed the equities of US asset managers for 10 years (2011 to 2021), though they have underperformed since the Covid-19 pandemic, the war in Ukraine and the interest rate turnaround´.

ARC ALPHA Global Asset Managers

ARC ALPHA Global Asset Managers is the only UCITS equity fund that invests exclusively in publicly listed asset managers. The portfolio contains around 35 equally weighted stocks. In addition, it has an equal geographical weighting between America and EMEA (with around 40% in each case), while asset managers in the Asia-Pacific region have a weighting of about 20%. Furthermore, the diversity of business models should be reflected in the portfolio – especially the weighting of traditional and alternative asset managers. Currently, about a third of the equities included in the fund are pure alternative asset managers. In addition, the fund holds the stocks of asset managers whose product range is spread across traditional and alternative asset classes. The fund always maintains an equity exposure close to 100%.

In the third quarter of 2024, the fund achieved a return of 7.66% (with a Sharpe ratio of 1.61). Over the past six months, the return amounted to 8.81% (Sharpe ratio of 0.93), and the year-to-date return totals 13.71% (Sharpe ratio of 1.05).

Frankfurt, 15 October 2024

If you have any questions, please contact:

Michael Klimek

E-Mail: mklimek@dolphinvest.eu

Tel.: +49 69 339978-14

_____________________________________________________________________________________________________________________________________

Disclaimer: The "Dolphinvest Global Asset Managers Barometer" serves information purposes only. The data, comments and analysis reflect the opinion of Michael Klimek, Managing Partner at Dolphinvest, related to the markets and their trends on the basis of his own expertise, economic analysis and information currently known to him. They shall not under any circumstances be constructed as comprising any sort of offer. All potential investors should consult their service provider or advisor and exercise their own judgement independently on the risks inherent to each investment and its suitability to their own personal and financial circumstances.

What is the Dolphinvest Global Asset Managers Barometer?

Each quarter we publish the “Dolphinvest Global Asset Managers Barometer”. This barometer is a tool for us to analyse the current situation of the asset management industry and to illustrate the view of international investors on the industry. For this reason, the “Dolphinvest Global Asset Management Barometers’” publication is by no means a buy or sell recommendation.

The barometer displays the performance of more than 100 listed asset management companies in EUR. For inclusion in the barometer, it is a mandatory requirement that a minimum of 75% of the overall revenue of a company is derived from asset management fees. Banks and insurance companies that have major asset management entities will, therefore, normally not be included in the barometer. The barometer represents all continents.

The transparency of listed asset management companies enables us to consolidate relevant information on the individual asset management companies included in the barometer into generally valid statements and to take them into account in our consulting work. Depending on the mandate, we divide the universe of constituents of the “Dolphinvest Global Asset Managers Barometer” into groups of similar companies against which we then benchmark our clients.

For a more detailed analysis and an interpretation of the findings, please contact:

Michael Klimek

Email: mklimek@dolphinvest.eu

Phone: +49 69 33 99 78 - 14