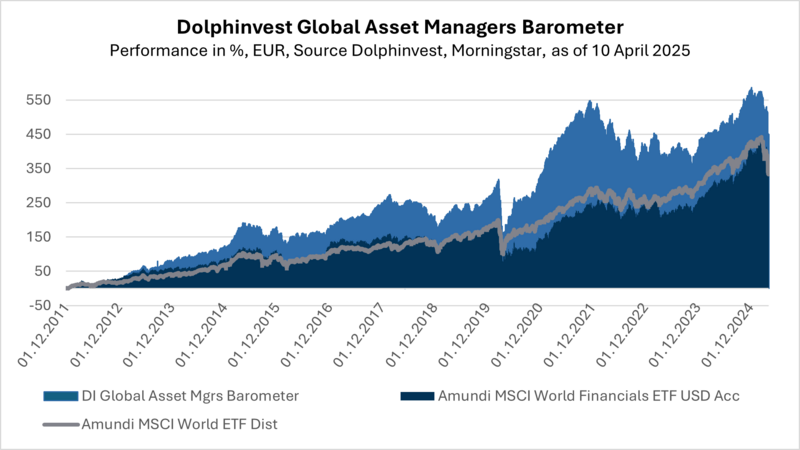

Dolphinvest Global Asset Managers Barometer

Protectionist EU economic policy: A case in favour

Ever since Donald Trump’s enthronement, the international capital markets have been under policy induced pressure. The result has been erratic ups and downs in the markets. What does this mean for the asset management industry?

For decades, the global equity and bond markets have grown, at regionally differing rates, through both up and down phases. Assets under management (AuM) have grown with them. Because when markets rise, there is an automatic increase in the value of client portfolios along with revenue from management fees.

But AuM don’t increase merely due to rising equity and bond prices. The globally increasing demand for asset management services also plays a role – which can be seen in the long-term historical development of stronger net inflows into funds.

The rising demand is based on intact secular demographic trends (growth of the world’s population and of the global middle class). This explains why the stocks of publicly listed asset managers have often outperformed the broader equity market over the long term in recent decades.

However, this doesn’t mean that there are no phases of underperformance by asset manager equities. Influencing factors that are detrimental to the industry include interest rate changes (especially restrictive monetary policy), economic problems, price and margin pressures, as well as government interventions in the market (over-regulation, but also the effects of decisions in other policy areas). At the present time, these influencing factors are all having a negative effect.

When investors flee from equities and go into bonds, bond prices rise due to the strong demand, and equity prices fall because of divestments. Since management fees for equity funds generally exceed those for fixed-income funds, asset managers ultimately earn less in such a situation.

But that’s not all. In the present market environment, investors have the choice between the devil and the deep blue sea. Either central banks raise interest rates in anticipation of accelerating inflation, which would be bad for bond prices and could also put pressure on equity prices – generally not good for asset managers and their clients. Or central banks fear an extended recession coupled with high inflation, which admittedly would reduce the likelihood of interest rate increases, but the prospects for equities would remain bleak in such a scenario. Sooner or later, the recession would cause rising unemployment, with less money to be save or invested.

All of this is currently taking place against the backdrop of price and margin pressures that have persisted for years in the industry, triggered by the triumph of passive investment strategies (i.e., ETFs).

Digression: Learn from Trump

EU citizens’ awareness of their inadequate defence capabilities was awakened only when US President Trump insisted – in an extremely unfriendly manner – on an increase in their defence budgets. The same demand was already made by his predecessors Barack Obama and Joe Biden, but evidently in an overly friendly way and was therefore ignored.

In this respect, the EU owes Trump the realisation that countries should not place their defence capabilities in the hands of other, temporarily friendly nations. Defence and security policy can only work reliably and responsibly in national self-sufficiency and independence. Fortunately, the long overdue political action has now been taken, not despite but due to Trump’s rude manner. This much self-criticism is necessary.

Trump has behaved in an almost ruder manner in the case of import tariffs on goods from other countries, including the EU. Here, Trump made several mistakes simultaneously, from which we can learn. Firstly, he underestimated the causes of the trade imbalances, such as the differences in price and performance of US and foreign cars, and the resultant strong US demand for Japanese, European and – little by little – Chinese cars, while foreign demand for US cars remained weak. So, it was completely pointless to impose tariffs on cars produced abroad because not one additional American car would be sold in the EU and elsewhere.

The second mistake was Trump’s sole focus on goods, and his failure to consider services in the current account balance. The US exports more services to Europe than Europe does to the US. If the conflict escalates further, the EU will respond very effectively, at some point, with tariffs on services and won’t be able to – or want to – limit itself to Google and Co.

Asset management is also among these services – and with much fewer price and performance differences than in the case of automobiles. Tariffs on management fees in funds (as well as indices) should be much more effective.

Redirect capital flows in two directions

Net securities investments as part of the capital account show a deficit for the EU. This means, except for the last quarter of 2024, EU investors invested more money outside the EU than within the EU in the four previous quarters: - 68.6 (Q4 2023), - 49.2 (Q1 2024), - 111.4 (Q2 2024), - 49.4 (Q3 2024) and + 82.4 (Q4 2024) (in billions of euros, respectively. Source: Eurostat). One reason for this is probably the MSCI World Index, the leading benchmark for the global equity market. At the end of March 2025, 72% of the index was allocated to the US alone; Japan, the UK and Canada made up a further 12.3% of the index. In other words, from every euro that flows from an investor in the EU into a fund or mandate with the benchmark MSCI World, 85% is invested outside the EU. This seriously cannot be in the interests of the European Union. Sound economic policy is something entirely different.

If the EU decides to impose tariffs on US asset managers – and if, for example, BlackRock’s ETFs in Europe become 20% more expensive – European investors will switch to the funds of Amundi, DWS and other European ETF providers. That’s no problem for EU investors. After all, the price – and only the price – determines success in the ETF business. Quality differences don’t influence the selection decision of investors, unlike in the case of US car drivers. The EU would have a bargaining tool here.

However, the European ETF providers also follow MSCI and other US-heavy indices. The order of the day must be to move away from market-weighted indices and to incentivise EU weightings due to the unequal sizes of the US and European capital markets. Alternative index offerings are needed to address the US’s unfair size advantage effectively. The Savings and Investments Union must make an economic policy contribution by making investments in the EU the rule, and investments outside the EU the exception.

But what if Trump then introduced punitive tariffs on the US business of European providers? For the 2024 financial year, DWS reported commission income of EUR 650 million from its activities in North and South America, equal to 16.3% of its total revenues of almost EUR 4 billion. For comparison, BlackRock’s commission income from its European business in 2024 was almost 10 times greater, namely USD 6.1 billion. The revenues generated in Europe thus amounted to 30% of BlackRock’s total revenues of USD 20.4 billion.

Therefore, the winner in a tariff war in the asset management industry should be Europe because US asset managers have more to lose in Europe in absolute and relative terms than their European colleagues in the US. An anecdote on the side may illustrate BlackRock’s understandably strong interest in Europe: In 2020, BlackRock received an advisory mandate from the European Commission regarding the regulatory integration of greener and more social goals, which later elicited sharp criticism. The Süddeutsche Zeitung reported: “The Americans outdid eight competitors, partly because their offer of EUR 280,000 was very attractive.” It’s doubtful whether BMW or Toyota would ever have had a chance to be appointed by the White House as an advisor for US transport policy because they had demanded a very low fee for their efforts…let alone under Trump.

Learning from Trump means active economic policy to assert one’s own interests. But the measures should be effective and reasonable. The goal must be to steer capital investments into the EU and to support the Savings and Investments Union through tax incentives. The emerging harmonised EU capital market must still grow enormously to be on an equal footing internationally. A politely restrained economic policy is inappropriate under the present geopolitical conditions. It must serve protectionist and – in a broader sense – also defence policy goals. Trump’s goal to abolish free trade offers a historic opportunity for the European Union and the Capital Markets Union.

Frankfurt, 15 April 2025

If you have any questions, please contact:

Michael Klimek

E-Mail: mklimek@dolphinvest.eu

Tel.: +49 69 339978-14

_____________________________________________________________________________________________________________________________________

Disclaimer: The "Dolphinvest Global Asset Managers Barometer" serves information purposes only. The data, comments and analysis reflect the opinion of Michael Klimek, Managing Partner at Dolphinvest, related to the markets and their trends on the basis of his own expertise, economic analysis and information currently known to him. They shall not under any circumstances be constructed as comprising any sort of offer. All potential investors should consult their service provider or advisor and exercise their own judgement independently on the risks inherent to each investment and its suitability to their own personal and financial circumstances.

What is the Dolphinvest Global Asset Managers Barometer?

Each quarter we publish the “Dolphinvest Global Asset Managers Barometer”. This barometer is a tool for us to analyse the current situation of the asset management industry and to illustrate the view of international investors on the industry. For this reason, the “Dolphinvest Global Asset Management Barometers’” publication is by no means a buy or sell recommendation.

The barometer displays the performance of more than 100 listed asset management companies in EUR. For inclusion in the barometer, it is a mandatory requirement that a minimum of 75% of the overall revenue of a company is derived from asset management fees. Banks and insurance companies that have major asset management entities will, therefore, normally not be included in the barometer. The barometer represents all continents.

The transparency of listed asset management companies enables us to consolidate relevant information on the individual asset management companies included in the barometer into generally valid statements and to take them into account in our consulting work. Depending on the mandate, we divide the universe of constituents of the “Dolphinvest Global Asset Managers Barometer” into groups of similar companies against which we then benchmark our clients.

For a more detailed analysis and an interpretation of the findings, please contact:

Michael Klimek

Email: mklimek@dolphinvest.eu

Phone: +49 69 33 99 78 - 14