Dolphinvest Global Asset Managers Barometer

Opportunities for everyone

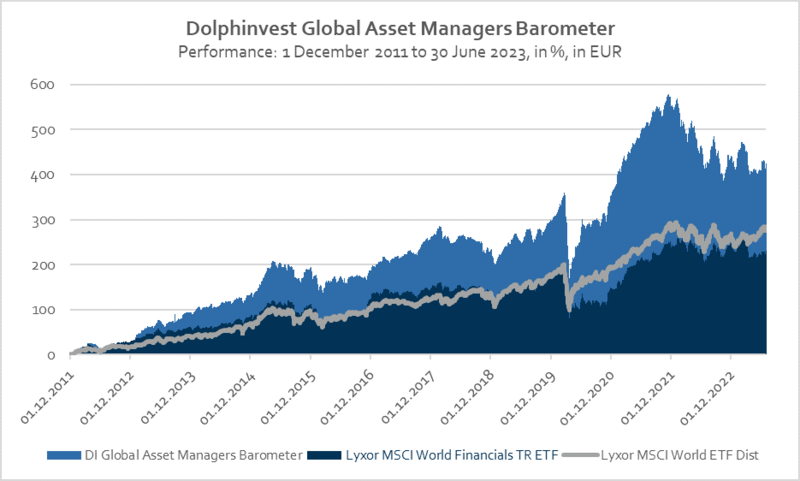

Some equity investors want to increase their capital, while others want to generate income. The segment of publicly listed asset management companies offers both types of investors interesting opportunities. In the second quarter of this year, for example, four Indian asset managers dominated the global competition and were among the Top 10 performers with gains exceeding 20% (in EUR). Two of them even managed gains of more than 35% on a three-month basis. This allowed the Dolphinvest Global Asset Managers Barometer to rise to 3.48 %. The ARC ALPHA Global Asset Managers, however, was unable to profit from this development because the fund – while investing globally in publicly listed asset managers – has shied away from investments on the sub-continent so far due to the disproportionately high trading costs, especially in India. Prime Minister Modi’s policy of opening India to foreign investors still has a lot of room for improvement.

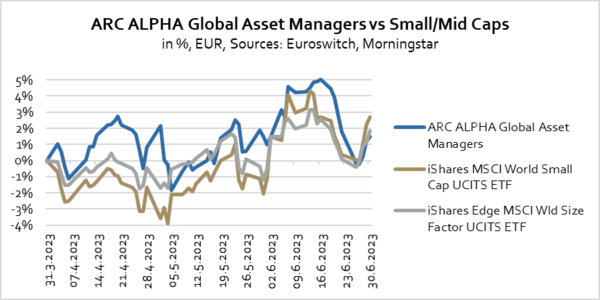

The announcement of the US Federal Reserve on 14 June that it would carry out even more interest rate increases in the second half of 2023 caused small and mid-cap stocks – which represent the

majority of publicly listed asset managers – to plummet. While rising interest rates are good for traditional banking business, they have a negative effect on the fixed income holdings of asset managers and on the returns from these investments. But equities can also be affected negatively by an environment of rising interest rates, which are typically less well tolerated by small companies than by large ones. Even though asset managers are generally less reliant on debt and bank financing than small-cap companies from the real economy, they nevertheless experienced a negative spillover effect.

How strong a rebound will turn out to be and when it will begin, depends on inflation expectations and on further interest rate developments. Optimists may already sense a buying opportunity because the earnings-based valuations of the asset management industry are in line with the financial sector overall, but have increased somewhat. The earnings-based valuations (see price-to-sales chart) converged with those of the real economy and financial sector until mid-2022; have risen slightly again since then; and should therefore provide stronger upside potential when interest rates stabilize or decline. Much depends on whether the peak of the interest rate cycle has been reached, and when the majority of equity analysts begin to price this into their models and lower the discount rate when calculating company valuations. At the moment, the market still appears to be waiting for a clear signal.

Cash is king – and the king is French

Besides providing the right to have a say on annual general meetings, equities grant shareholders the right to participate in dividend payments. For one, equities are currently becoming more attractive as an instrument of wealth creation among politically motivated investors because the use of co-determination rights at shareholder meetings makes it possible, for example, to influence the environmental policies of companies.

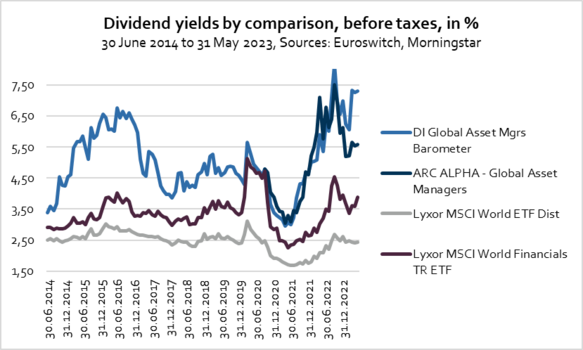

In addition, dividends offer private investors the possibility – just like with bonds or property ownership – to generate additional income and to create a broader income base. For years, the asset management industry has been among the ‘high-flyers’ for dividend yields compared with both the real economy and the financial sector. With an investment in this sector, equity investors have been able to generate attractive income in the past because asset management is considered ‘cash-rich’ due to optimal payment streams, and debt service is hardly known.

At the end of May 2023, the median market capitalisation of asset management companies stood at EUR 818 million, while the dividend yield covering the previous 12 months was 5.3%. By comparison, in May 2021, the dividend yield amounted to 3.9% with a median market capitalisation of EUR 1,097 million. Therefore, assets under management declined, while dividends rose, in parallel with inflation and interest rate developments.

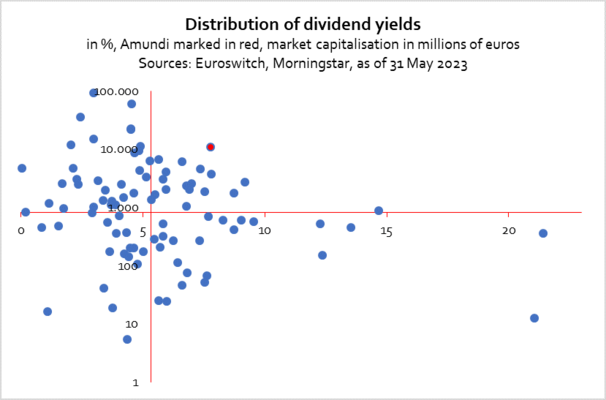

As the only large company with a market capitalisation of more than EUR 10 billion, the French asset manager Amundi achieved a dividend yield above the median (marked red in the chart) this year. The company therefore occupied a leading position not only compared with other industry giants, but also in the overall competitive environment. In the comparable period two years ago, Amundi was already No. 1 for dividend yields in the large-cap group.

Frankfurt, 17 July 2023

If you have any questions, please contact:

Michael Klimek

E-Mail: mklimek@dolphinvest.eu

Tel.: +49 69 339978-14

_____________________________________________________________________________________________________________________________________

Disclaimer: The "Dolphinvest Global Asset Managers Barometer" serves information purposes only. The data, comments and analysis reflect the opinion of Michael Klimek, Managing Partner at Dolphinvest, related to the markets and their trends on the basis of his own expertise, economic analysis and information currently known to him. They shall not under any circumstances be constructed as comprising any sort of offer. All potential investors should consult their service provider or advisor and exercise their own judgement independently on the risks inherent to each investment and its suitability to their own personal and financial circumstances.

What is the Dolphinvest Global Asset Managers Barometer?

Each quarter we publish the “Dolphinvest Global Asset Managers Barometer”. This barometer is a tool for us to analyse the current situation of the asset management industry and to illustrate the view of international investors on the industry. For this reason, the “Dolphinvest Global Asset Management Barometers’” publication is by no means a buy or sell recommendation.

The barometer displays the performance of more than 100 listed asset management companies in EUR. For inclusion in the barometer, it is a mandatory requirement that a minimum of 75% of the overall revenue of a company is derived from asset management fees. Banks and insurance companies that have major asset management entities will, therefore, normally not be included in the barometer. The barometer represents all continents.

The transparency of listed asset management companies enables us to consolidate relevant information on the individual asset management companies included in the barometer into generally valid statements and to take them into account in our consulting work. Depending on the mandate, we divide the universe of constituents of the “Dolphinvest Global Asset Managers Barometer” into groups of similar companies against which we then benchmark our clients.

For a more detailed analysis and an interpretation of the findings, please contact:

Michael Klimek

Email: mklimek@dolphinvest.eu

Phone: +49 69 33 99 78 - 14